The Truth About Money

You may have heard that it’s best to have the smallest mortgage you can and to pay it off as quickly as possible. Or perhaps you have heard to save up as much money as you can to throw it all at your down payment. Many people don’t fully understand the benefits of a mortgage, and there is a lot of misinformation about them. We highly recommend checking out financial guru Ric Edelman’s book The Truth About Money where he explains these 11 reasons you should have as big and long of a mortgage as you can.

This is just a synopsis from Edelman’s book, be sure and check it out in it’s entirety here.

Reason #1 Your Mortgage Doesn’t Affect Your Home’s Value

Many people buy a home because they think it will rise in value over time. In fact, it will rise and fall in value many times over the next 30 years. This will occur whether you have a mortgage or not. Your home’s value is unaffected by the mortgage against it. That is why owning your home outright or putting up a large down payment is like stuffing money underneath your mattress. The home’s value with grow regardless if it has a mortgage or not, so the equity you currently have in your home is earning essentially no interest. Having a long-term mortgage lets your equity grow as your home’s value does.

Reason #2 A Mortgage Won’t Stop You From Building Equity In The House

One of the main financial reasons for owning a home is to gain equity. Many people say mortgages are bad because the bigger the mortgage, the lower your equity. They’re wrong and here’s why.

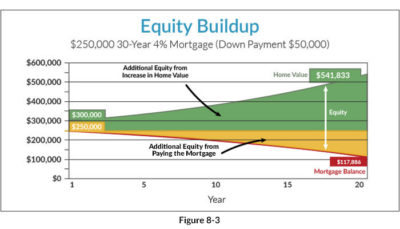

Say you buy a house for $300,000, and you get a $250,000 30-year 4% mortgage. Your down payment ($50,000 in this example) is your starting equity, and you want that equity to grow, grow, grow.

By making your payments each month, your loan’s balance in 20 years will be just $117,886. This supports the contention that equity grows as you pay off the mortgage and that, therefore, the faster you pay off the mortgage, the faster your equity will grow.

But this thinking fails to acknowledge that this is not the only way you will build equity in your house. That’s because your house is almost certain to grow in value over the next 20 years. If that house rises in value at the rate of 3% per year, it will be worth $541,833 in 20 years! You’ll have nearly a quarter million dollars in new equity even if your principal balance never declines!

Reason #3 A Mortgage Is Cheap Money

Mortgages, in fact, are the cheapest money you will ever be able to borrow. (Oh, sure, you can get a credit card that offers 0% interest for six months, but try to borrow a couple hundred thousand for 30 years that way.)

You get a loan when you demonstrate you have the ability to repay it. But how much interest will you have to pay? The more confident the lender is that it will get its money back, the less interest it will charge you. By offering your house as collateral, you agree to let the bank have your house if you don’t repay the loan. This dramatically reduces the bank’s risk, resulting in a very low interest rate. (By contrast, credit cards have no collateral; Visa can’t take the sweater you bought if you don’t pay the bill. Credit card companies know that a certain portion of their cardholders will default, so they charge 18% to most cardholders. They figure that if a third of the cardholders default, they’ll still end up with a 12% return on their money. Not a bad business.)

Reasons #4 and #5 Your Mortgage Interest Is Tax-Deductible. And Mortgage Interest Is Tax-Favorable.

Mortgages, in fact, are the cheapest money you will ever be able to borrow. (Oh, sure, you can get a credit card that offers 0% interest for six months, but try to borrow a couple hundred thousand for 30 years that way.)

You get a loan when you demonstrate you have the ability to repay it. But how much interest will you have to pay? The more confident the lender is that it will get its money back, the less interest it will charge you. By offering your house as collateral, you agree to let the bank have your house if you don’t repay the loan. This dramatically reduces the bank’s risk, resulting in a very low interest rate. (By contrast, credit cards have no collateral; Visa can’t take the sweater you bought if you don’t pay the bill. Credit card companies know that a certain portion of their cardholders will default, so they charge 18% to most cardholders. They figure that if a third of the cardholders default, they’ll still end up with a 12% return on their money. Not a bad business.)

Reason #6 Mortgage Payments Get Easier Over Time

Carrying a mortgage actually gets to be fun. Yes, fun. My father used to love to talk about his mortgage — all $98 per month of it. You see, he and my mom bought their home in 1959 for the whopping price of $19,500! Yet, my dad used to tell how his father thought he was crazy. How in the world was my father going to be able to handle such a huge mortgage payment, Grandpop Max asked. After all, my father was earning less than $3,000 a year back then. To spend $1,200 a year on mortgage payments … Grandpop Max thought my dad was nuts!

Of course, by the 1970s, Dad was laughing about it. Why? Because his monthly payment in 1974 was identical to what he was paying back in 1959. Yet, Dad’s income had risen steadily. Thus, his mortgage payment had become insignificant when compared to his income — not to mention the fact that his house had grown substantially in value.

You probably remember struggling to make your mortgage payment when it was new. But over time, that payment becomes cheaper relative to your income — especially if yours is a fixed-rate loan: Payments on such loans will never rise but incomes usually do.

Reason #7 Mortgages Allow You To Sell Without Selling

Have you noticed that your home is worth much more than it was 10 years ago?

You might be worried that your home’s value will fall.

If you’re afraid that your home’s value might decline, you should sell the house before that happens. But you don’t want to do that! It’s your home, after all. You have roots in the community. Uproot the kids? And where would you move? No, selling is not a practical idea.

Still, you fret that your home’s equity is at risk. Can you protect it without having to sell? Yes! Simply get a new mortgage, and pull the equity out of the house. It’s the same thing as selling, except that you don’t have to sell!

Here’s how the idea works: Say you bought a house for $200,000 with no money down (meaning you owe the bank $200,000). Further say that prices have skyrocketed, and houses in your neighborhood have been selling for $500,000. You fear that prices will fall, dropping your home’s value to $400,000.

If you sell now for $500,000, (Assuming that you can, and ignoring real estate commissions and other selling expenses, and pretending that you still owe the bank the full amount of the original $200,000 loan.) you’d pocket $300,000. But you don’t want to sell, so just refinance and get a new loan for $500,000. You now have the $300,000 in hand — just as if you had sold the house! Obviously, this is an extreme example simply to prove a point. I’m not necessarily suggesting you actually get a new mortgage that’s two-and-a-half times bigger than your old one – although I might, depending on the situation. And don’t forget the tax limitations regarding the deductibility of the large new loan.

Borrow the money now, because you won’t be able to do so after the house falls in value.

I’m not suggesting that you’d want to owe more on the house than the house is worth. But that’s certainly better than watching the equity evaporate before you have a chance to use it.

Reasons #8 and #9 Mortgages Allow You To Invest More Money And To Invest It More Quickly. Mortgages Allow You To Create More Wealth Than You Otherwise Would.

As I mentioned in Reason #6, people get big mortgages on their first home simply because they don’t have a choice. You’re excited about buying a house, and even though you don’t have much money, you have a good income — two good incomes, if you’re like many couples. Some years later, with a growing family, higher incomes, and newfound equity in the house, you’re ready to move up to a bigger home.

Let’s say you net $300,000 from the sale of your old house, and you’re ready to buy a new home for $300,000.

Should you use all your cash and make a $300,000 down payment? Or should you place only $60,000 down, which is 20% of the purchase price?

If you make the bigger down payment, your monthly mortgage would be $1,146, assuming a 4% 30-year mortgage.

This explains why so many people prefer to make big down payments when they buy houses. A big down payment translates to a small monthly payment.

But the people who are trying to ask you to choose between big monthly payments and small monthly payments are lying to you. Yep, they’re tricking you by asking you the wrong question.

The correct question is not about the amount of money you want to pay monthly, but the amount you want to invest. Again, it’s all about wealth creation, not debt elimination.

Here’s the question you should be answering:

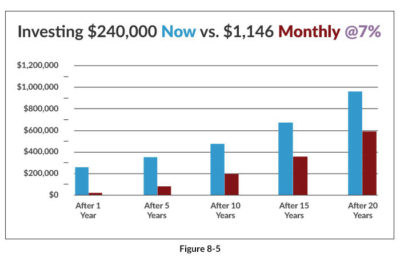

Would you rather invest:

$240,000 right now, as a one-time-only deposit

or

$1,146 a month, every month, for the next 30 years?

Obviously, you’d prefer the strategy that results in a higher profit. And Figure 8-5 reveals the answer. Regardless of the time period, investing a large amount now produces better results than investing small amounts over long periods.

Thus, while a low mortgage payment lowers your overall expenses, it also lowers your overall wealth.

But you suspect there’s a flaw here. In order to invest that $240,000, you’d have to be willing to accept the higher monthly payment. Where will you get the money to do that each month?

You’ll find the money from two places. First, increase your paycheck! Remember that the new loan payments are almost entirely tax-deductible interest. That means you don’t need to have as much money withheld from your paycheck. So file a new IRS Form W-4 at work to increase your exemptions; this will reduce the amount of taxes that are withheld from your paycheck, boosting your net pay. Yes — you’ve just given yourself a raise! And you can use this increased paycheck to help you pay for your new mortgage payment.

Second, if your paycheck isn’t enough, simply make periodic withdrawals from the investment account you’ve just created. Soon enough, as your income rises, you won’t need this crutch; your income will become enough to handle the cost, as shown in Reason #6.

In fact, getting a big mortgage and using investment proceeds to help you make the payment is superior to getting a small mortgage and having no proceeds to invest. This is especially true when you discover the most important reason of all to carry a big, long mortgage…

Reason #10 Mortgages Give You Greater Liquidity And Flexibility

To help you understand this, let me introduce you to Nervous Nick and Smart Sam.

They have the same income and expenses, and are in the 25% tax bracket. Each has $100,000 in cash; each wants to buy a $300,000 house.

Smart Sam gets a $240,000 30-year mortgage at 4%. He makes no extra payments. But Nervous Nick takes a different approach. Nick hates mortgages and wants to get rid of his mortgage as quickly as he can. He fears that if he has a mortgage, he might one day lose his house. He doesn’t quite understand how that could actually happen, but his granddaddy told him that mortgages are bad, and Nick believes his granddaddy, so he goes with a small mortgage — as small as possible. That means he uses his entire $100,000 in cash to make a down payment. His mortgage is therefore smaller than Smart Sam’s — $200,000.

Nervous Nick also gets a 15-year loan instead of a 30-year loan, because he hates mortgages and he figures the 15-year loan will let him get rid of his loan in half the time. Nick also knows that this clever ploy garners him a lower interest rate, because lenders charge less for 15-year loans than they charge for 30-year loans. So while Sam is paying 4%, Nick is paying only 3.5%.

Nick, in fact, is so obsessed with getting rid of his mortgage that every month he sends an extra $100 to his lender. He knows that the more he sends in, the faster his loan will be paid off. So, compared to Sam, Nick has a smaller mortgage, a shorter mortgage, a lower interest rate — and he’s adding money to each payment.

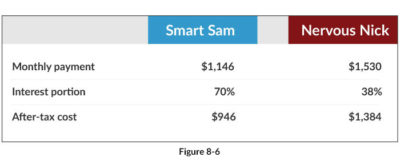

Figure 8-6 shows where the two men stand. Smart Sam’s monthly payment is $1,146. Thanks to amortization, almost all of Sam’s payment — 70% of it — is comprised of interest. Thus, on an after-tax basis in the 25% federal income tax bracket Smart Sam’s payment costs him $946 a month.

Meanwhile, Nervous Nick’s payment is $1,530 a month. But only 38% is interest. That’s because Nick’s loan is for 15 years: The shorter the term, the more principal you must pay each month, and principal payments are not tax-deductible (only the interest is deductible). So even though Nervous Nick is paying more per month than Smart Sam, he’s deducting less. Nick’s after-tax cost, therefore, is $1,384.

Thus, Smart Sam is paying $438 less per month than Nervous Nick. But Nick doesn’t mind. He doesn’t mind the extra monthly cost because he knows he’ll get rid of his mortgage quicker.

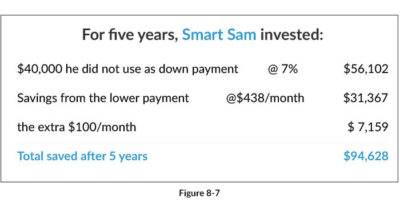

So for the next five years, Smart Sam makes his monthly mortgage payments. And instead of sending an extra $100 every month to his lender like Nick does, Sam puts that $100 into exchange-traded funds. Then both men lose their jobs. Or perhaps one develops a medical condition, or his wife has a baby and quits work. Whatever the cause, something happens in five years that causes their income to fall or expenses to rise — or both. Figure 8-7 shows Sam’s status.

Nick’s been busy paying down his mortgage; the outstanding balance is only $149,000. But does that matter? The guy just lost his job, but he still has to make his monthly mortgage payment. So it doesn’t matter that his mortgage balance is $149,000; what matters is that his mortgage payment of $1,5301 is due at the end of the month.

This is a real problem for Nick, because with no job, he has no income. He also has no money, because he’s given every available dollar to the bank in the form of extra payments. Nervous Nick’s nightmare is coming true! He’s about to lose his house!

Sam, though, is in much better financial condition. Oh, sure, his mortgage balance is higher than Nick’s but does that matter? Not at all. What matters is that he has to find some way to make his $1,146 payment.

But Sam is not in the same predicament as Nick. That’s because Sam has lots of savings, as shown in Figure 8-7. First, he gave the bank a smaller down payment, enabling him to invest $40,000. Based on an average annual return of 7%, that money grew to $56,102.

Smart Sam also took advantage of the fact that his monthly payment was $438 less than Nick’s; he invested that money too, which is now worth $31,367. And instead of sending $100 a month to his lender like Nick, Sam added $100 to his investments; those investments are worth $7,159. All told, Smart Sam has $94,628. So even though he’s out of work, he’ll be able to make his mortgage payments for another six years!

How ironic that Nick, who wanted to get rid of his mortgage so he wouldn’t lose his house, is about to suffer the fate he was so desperately trying to avoid. This fable shows you why it is so important that you minimize both your down payment and your monthly payment. By doing so, you retain more of your money.

By keeping control over access to your money, you maintain liquidity. But when you give your money to your lender, you lose control of it. After giving money to your lender, the only way to get your money back is to sell the house — and that’s the one thing Nervous Nicks does not want to do.

This reveals the fatal flaw in the logic of those who lie to you about mortgages. Sure, owning a home mortgage-free is an appealing concept. But it is completely unrealistic! I mean, sure, paying off your mortgage is great — if that’s the only thing you need to do with your money. But what about paying for college? Saving for retirement? Caring for elderly parents? Or even just paying for car repairs!?!?

Indeed, the fatal flaw of those who tell you to do everything you can to pay off your loan as quickly as you can is that they are completely ignoring everything else that’s happening in your life! If you succeed in paying off the loan, you might fail in paying for college, or covering costs in the event of a job loss, medical problem, marital issue, or other family concern.

That’s why you must stop listening to those who pretend that the only thing that matters is paying off a mortgage. Your life is more complicated than that, and by realizing this, you see that trying to pay off the mortgage like Nervous Nick is actually a risky thing to do. Instead, the smarter and safer approach is to carry a big, long mortgage and don’t bother trying to pay it off!

Reason #11 You’ll Never Get Rid Of Your Monthly Payment, No Matter How Hard You Try

You want to eliminate your mortgage so that you don’t have to make any payments in retirement. That’s too bad, because even if you somehow eliminate your mortgage, you won’t eliminate your payments.

Sure, paying off your mortgage means you no longer make any principal or interest payments. But mortgages are known as PITI, and we’ve only addressed the P and the I. Let’s not forget about the T and the other I — or the M and the R.

I’m talking about taxes and insurance. Even if you manage to pay off the loan, you’ll still have to pay property taxes and homeowner’s insurance. Thus, your goal of “getting rid of the mortgage payment” is impossible! Even if you eliminate the mortgage, you’ll still have tax and insurance payments.

And as long as you own your house, you’ll have Maintenance and Repairs to contend with as well. So don’t bother trying to make your mortgage go away. Instead, create wealth so that you can comfortably afford the cost of living in and owning your home.

The above examples are for illustrative purposes only and do not fully take into account expenses such as property taxes or homeowner’s insurance. The examples used here assume that the rate of return on investments will be greater than the interest rate paid on a home mortgage. As there are risks with virtually any investment, there can be no assurance that you will achieve returns greater than the interest rate on your home mortgage. Changes in federal income tax laws could have adverse consequences for the mortgage interest deduction.

Taking equity out of your home involves risk, particularly in slow or declining markets. This could result in some homeowners owing more money than their home is worth. Even if your home sells for its appraised value, the net proceeds could be much lower than anticipated due to legal fees, realtor fees, and other closing costs. There is also the potential for a reduced tax deduction. Any amount that you borrow over 100% of equity is not tax deductible.

Originally published in The Truth About Money

Podcast: Play in new window | Download